Key facts

ProCredit at a glance

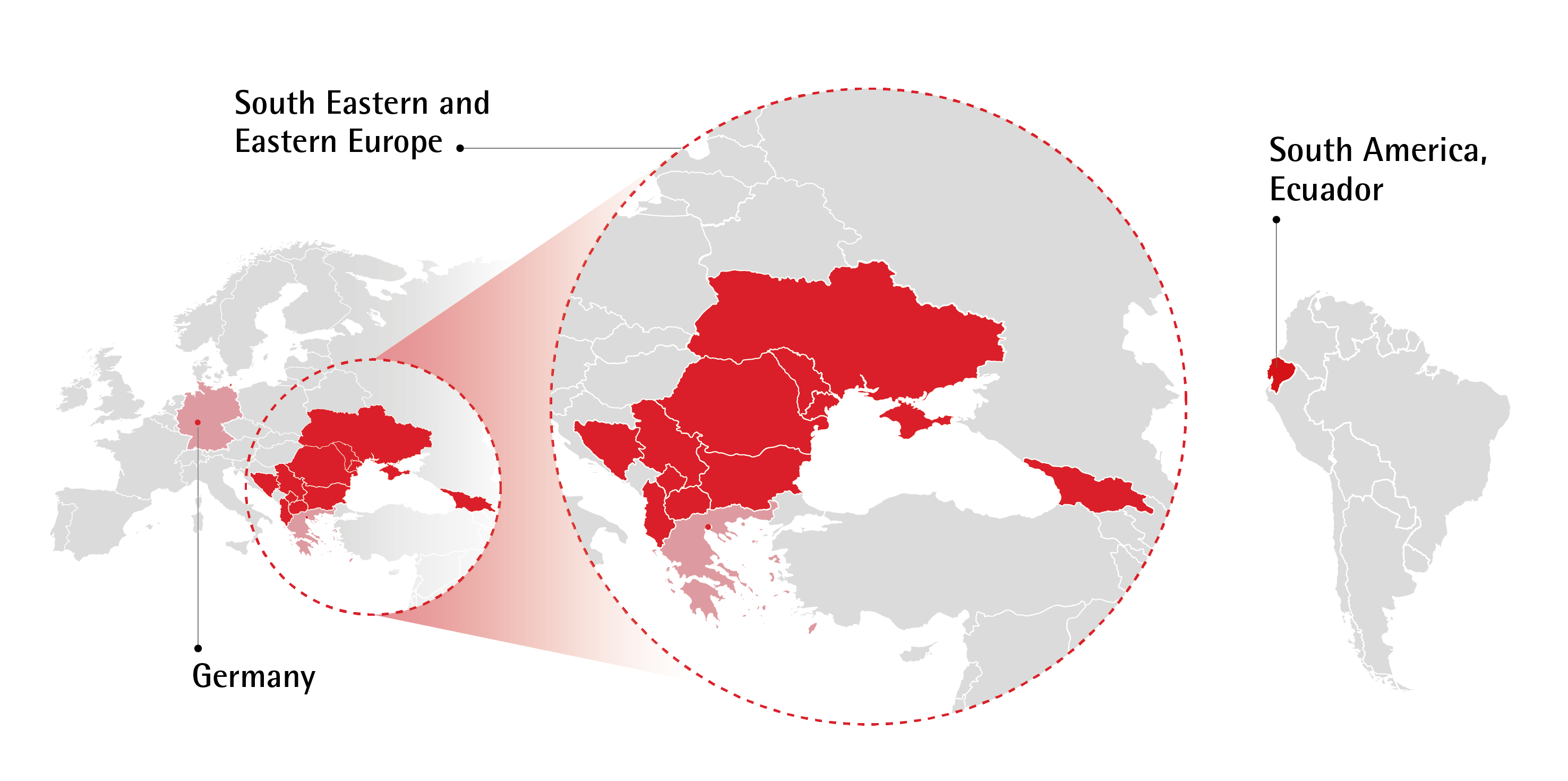

- An impact-oriented group of commercial banks with a focus on MSMEs and Private Clients in South Eastern and Eastern Europe

- “Hausbank” for MSMEs and ProCredit Direct for Private Clients

- Headquartered in Frankfurt and supervised by BaFin and Bundesbank

- Track record of high-quality loan portfolio based on prudent risk management and focus on long-term business relationships

- Profitable every year since creation as a banking group

Our Mission

We strive to be the leading SME bank in our markets following sustainable and impact-oriented banking practices. Together with our fully digital offering to private clients, we want to generate long-term sustainable returns and create positive impact in the economies and societies we work in.

Regional footprint

Key group figures

Key financials (in EUR million)

| FY 2022 | FY 2023 | |

| Total assets | 8,826 | 9,749 |

| Loan portfolio | 6,108 | 6,226 |

| Shareholders’ equity | 869 | 984 |

| Profit of the period | 16.5(1) | 113.4 |

Key metrics

| FY 2022 | FY2023 | |

| Net interest margin | 3.1% | 3.6% |

| Cost of risk | 174 bps (1) | 25 bps |

| Cost-income ratio | 64.0% | 59.9% |

| Return on equity | 1.9%(1) | 12.2% |

| CET1 ratio (fully-loaded) | 13.5% | 14.3% |

| Deposit-to-loan portfolio | 103.0% | 116.5% |

| Number of employees | 3,437 | 3,834 |

| Book value per share (EUR) | 14.8 | 16.7 |

(1) negatively impacted by significant loan loss provisions in Ukraine

Ratings

| FitchRatings | Long term rating (outlook) | BBB (stable) |

| MSCI ESG Research | ESG rating | A |

| ISS ESG | Corporate rating | Prime |